With Internetbanking, you have access to your account any time and you can conduct your financial transactions online, safely and easily at home.

The following functions are available:

Electronic bank statements and receipts

Free domestic and EU transfers

Opening Daily Savings Accounts and Time Deposit Accounts

High security with mobile TAN

Foreign transfers

Template management for recurring payments

Advanced search for account activities

Account balance queries

Update of contact details

New customers have to register under “Open New Account” on the DenizBank AG website. After successful registration and verification of your identity, the customers will receive their login information per post.

If you are already a DenizBank AG customer, please download the Internetbanking Application Form from our website and

send us the signed form per post.

Payment- or Daily Savings Account at DenizBank AG

An Email address

Internet access

A mobile phone number

Please use the button "Login Internetbanking" under Private” on the DenizBank AG website to go to

the login page of DenizBank AG Internetbanking. There you need to enter your customer number and your PIN. Joint

account holders have to enter both, the joint account number as well as the private customer number.

New customers receive their log-in data as soon as all their documents are complete at DenizBank AG. For customers who have registered online, DenizBank AG has to wait for the confirmation of identity verification by the Deutsche Post AG.

Your PIN will be sent via SMS to the mobile phone number you have registered at DenizBank AG.

When entering your log-in data, please use your own keyboard and make sure you pay attention to upper and lower case letters. In addition to this, when you first log in using the PIN you got from DenizBank AG, you need to change your PIN into a personal on

New log-in data can only be ordered in written form. Please use the Internetbanking Application Form under “Customer Service

/ Documents”. Please return the signed application form per post or visit one of our branches

With an "Own Account Transfer" you can transfer your savings between your Payment Account and your Daily Savings

Account. This feature can be found in the Internetbanking

under

"Transfers“.

No, "Own Account Transfer" enables you only transactions between your DenizBank AG accounts.

Choose the function “Transfers” in the Internetbanking.

Please note that transfers are only possible from your Payment Account.

DenizBank AG offers this service to its customers free of charge as long as the transaction is made online.

With the “Foreign Transfers“ feature, you can also accomplish transfers outside the EU.

Yes, international transfers are charged with a fee. The current prices for foreign transfers are

listed in our List of Fees.

You can only conduct external transfers from your Payment Account. Please transfer your deposit from your Daily Savings Account to your Payment Account by using the function "Own Account Transfer“. The transfer is completed within a few minutes, so you can conduct further transfers immediately.

Online Savings

Online Deposit Accounts

You can either register on the homepage of DenizBank AG and apply for an account or visit one of our our branches.

Once you have registered on the homepage, you will receive the application form by Email The signed application and the Post-Ident-Coupon have to be sent to DenizBank AG by mail so that the verification of identity is executed by the post office.

General terms and conditions and a copy of account openning form should be retained for your documents.

Once we have received these documents, you will get your log-in data via text message sent to the mobile number you have entered in the application form.

This account enables you to open deposits and offers you additional transfer functions. A Payment Account should not be mistaken with a Daily Savings Account. From your Payment Account, you can open Daily Savings and Time Deposit Accounts. Therefore, the deposit of an external Reference Account is not required.

The prevention of money laundering act (Geldwäschegesetz GWG) obliges us to verify the identity of our customers when opening an account. The PostIdent-Coupon is the most convenient method to verify your identity. You will receive a printed PostIdent-Coupon together with your application documents. You will need to sign this form upon receipt of the application documents at the post office. The PostIdent-Coupon will then be sent to DenizBank AG by post.

You can withdraw money in all of our our branches . Please transfer your money from your Daily Savings to your payment account beforehand.

Payment Account

This is a base account which enables you to open deposits and offers you additional transfer functions. A Payment Account should not be confused with a Daily Savings Account. From

your Payment Account, you can open Daily Savings and Time Deposit Accounts.

Therefore, the deposit of an external Reference Account is not required.

If you are already an online customer at DenizBank AG, you can open a Payment Account in the Internetbanking Portal of DenizBank AG under “Account Management

/ Online Deposits”.

DenizBank AG offers the Payment Account free of charge. Online transactions within Germany and EU are free of charge as well.

The interest rate is 0.01% p.a. The account statement is issued quarterly.

The Payment Account is used as a Reference Account for your deposits and money transfers. In order start saving, you have to open a Daily Savings or a Time Deposit Account in your Internet Banking Account.

Daily Savings Account

The Daily Savings Account is an Online Deposit Account of DenizBank AG. It offers you

attractive interest rates and instant access to your savings.

The Daily Savings Account is only offered to customers with Internet Banking.

Customers with a Payment Account can open a Daily Savings Account using the “Account Management“ and “Online Deposits“ functions in Internet Banking.

The current interest rate of the Daily Savings Account you can find in the list of fees

DenizBank AG offers you the Daily Savings Account free of charge.

DenizBank AG offers you the opportunity to open only one Daily Savings Account.

The minimum deposit is 100 Euro.

You can transfer your deposit directly to your Payment Account. The next step is to open a Daily Savings Account

and transfer the deposit amount onto the Daily Savings Account. You can also deposit your Payment Account at one

of our branches.

Transfers from your Daily Savings Account are not possible. Please use your Payment Account for this purpose. By using “Own Transfer”, you can transfer your deposit from your Daily Savings Account to your Payment Account from where you can conduct further transfers to external accounts.

On December 31st of each year, the accumulated interest will be credited to your Daily Savings Account.

Time Deposit Account

The Time Deposit Account is an Online Deposits Account at DenizBank AG. A specific amount (minimum amount 1.000 Euro) is

invested for a fixed term with fixed interest rates for the whole term. At maturity the interest will be credited to

your account.

You can open the Time Deposit Account in your Internetbanking account under Online Deposits/Open a Time Deposit

Account.

Please enter the deposit amount, the debit account (either Payment Account or Daily Savings Account) and the

roll

over type and confirm your entries with a TAN.

Please log- in the Internetbanking and go to ''Account Management''. Then you choose ''Online Deposits“ and ''Open a Time Deposit Account“. Enter the deposit amount, the debit account (Payment Account or Daily Savings Account of DenizBank AG) and the roll over type. Then confirm your entries with a TAN.

Please note that the deposit must be on your Payment or Daily Savings Account before you open a Time Deposit

Account.

DenizBank AG offers the following terms:

3 Months

6 Months

9 Months

12 Months

18 Months

24 Months

32 Months

48 Months

60 Months

72 Months

84 Months

96 Months

108 Months

120 Months

The minimum deposit amount is 1.000 Euro.

Please transfer your deposit to your Payment Account and open a Time Deposit Account online.

Interest amount is paid out to the payment account at the end of the term. With terms of more than one year, interest amount is credited annually.

For opening a Time Deposit Account, you need to have a Payment Account at DenizBank AG. The deposit you want to invest on your Time Deposit Account has to be already on your Payment Account.

It should also be noted that you have to choose the roll over type:

Re-payment at maturity

The amount will be transferred to your Payment Account at maturity.

Re-invest of interests and capital:

The interests and capital will be reinvested for the same term with the interest rate applicable at the time of

maturity.

Re-invest of capital:

The capital will be reinvested for the same term with the interest rate applicable at the time of maturity. The

interests will be transferred to your Payment Account.

You can open an unlimited number of Time Deposit Accounts at DenizBank AG.

According to the roll over option you have chosen, your time deposit is either transferred to your Payment Account or prolonged/re-invested (only principal amount or principal together with the interest amount).

If you do not want to re-invest a written notification is required.

The interest rate of a Time Deposit Account is guaranteed for the whole term.

Time Deposit Account is free of charge.

An early cancellation of Time Deposit Account before maturity is excluded for both sides and can be made only in exceptional individual cases.

In the event of early termination, the interest rate is retrospectively reduced to 0.0% p.a. and a deduction of interest on advances made in favor of the bank. The advance interest exceeds the agreed credit interest rate by a quarter (as of August 2019). In addition, due date fees apply according to our list of fees.

smsTAN Verification

A TAN (transaction number) is a one-time password (OTP) used in Internetbanking to verify transactions.

The smsTAN Verification is a two-way authorization procedure. When you want to place an order you receive your TAN only if required via SMS directly to your mobile phone. . This TAN is valid only for a few minutes and just for this transfer. The transaction will be completed after entering the TAN into the specified field.

The delivery of the SMS is free of charge. Please note that when a smsTAN is delivered abroad, a roaming fee may be charged by your provider.

You can choose one of 3 options to change your phone number:

a. By post

Just send an informal signed letter with your new phone number to DenizBank AG, Frankfurt Münchener Strasse 7, 60329 Frankfurt/Main.

b. Per Fax

If you have indicated during the account opening that you also want to give orders by fax, you can change your

number in this way.

c. In a branch

You can also visit us in one of our 3branches all over Germany. Our staff will be happy to assist you.

S€PA – Payment transactions without borders

SEPA (Single Euro Payments Area) is standardizing cashless payment transactions within Europe.

The participating countries include the 28 EU Member States plus Norway and Liechtenstein as Member States of the European Economic Area (EEA), together with Monaco and Switzerland.

As of 1 February 2014, SEPA will likewise change the cashless payment transaction system in Germany. Banks and savings institutions (Sparkasse) are required to execute transfers and direct debits made in Euro in accordance

with a standardized European-wide scheme.

The IBAN (International Bank Account Number) replaces your account number; the BIC (Business Identifier Code) replaces your bank code.

Would you like more information about SEPA or do you have any particular questions?

For more information, please read

FAQ Private Customers

The conversion to the single payment area affects everyone who has an account with a Bank – irrespective of whether they are an individual person, an association, an enterprise or a public institution.

The SEPA conversion will not cost private customers anything.

Yes, SEPA means more security for payment transactions. Take direct debit collection mandates for example - the payee can be unambiguously identified through the new creditor identifier. Assigned in Austria by the Oesterreichische Nationalbank, the consumer can see the creditor identifier both in the SEPA direct debit collection mandate and in the account statement – or online in the account payments history display, all of which creates greater transparency.

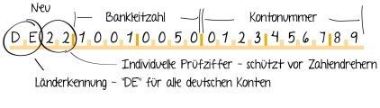

TheIBAN is easy to notice, because it is made up of the 10-digit account number and the 8-digit bank (sort) code, together with the national code DE for Austria and a 2-digit verification number. That means that, other than these four characters, the IBAN is uniquely assigned to you.

Quelle: Österreichische Nationalbank

Your new, 22-digit account number is now displayed on your account statements (top right-hand corner). When banking online, you can get your IBAN at »Account Management« › »Account Information« › »Account Detail«. Or use our free smartphone app with its practical IBAN computer – simply enter your account number and you're good to go!

The international exchange of data between banks is regulated by the "Society for Worldwide Interbank Financial

Telecommunications" (SWIFT). It assigns every participating bank a unique international bank ID, known as the "Bank

Identifier Code" (BIC). The BIC consists of eight or eleven characters. It is made up of

the 4-digit bank code

the 2-digit country code

the 2-digit location code

the 3-digit code for the branch or department (optional).

No, we will convert your standing orders to be ready for SEPA.

Starting from 1 February 2014, you will begin using the IBAN instead of your previous account number and bank code. The IBAN is sufficient when making payments inland (BIC not needed). The BIC will still be needed when making international payments (foreseeably until February 2016).

Cross-border transfer charges are more cost-effective with SEPA - a SEPA transfers costs the same as an inland bank transfer, dependent of course on the specific terms of the particular account.

No, they are the same. Within the Eurozone, the transferred sums have to arrive in the target account within one banking day.

There is a new pre-printed form for Euro transfers, which you can obtain in our branch offices. You can also make payments easily using your online banking access.

Within Germany, goods and services are frequently paid for using a direct debit collection mandate (Einzugsermächtigung). As a consumer, you will certainly be familiar with these when making payments to your energy supplier. For the first time, the new SEPA Direct Debit Scheme enables due invoiced sums to be collected by direct debit not only with Germany, but also across borders within SEPA. Payees that use the SEPA direct debit method will need you to provide them with a SEPA direct debit collection mandate. However, as the payer there is no need for you to act. It is the responsibility of the payee to approach you to obtain the direct debit collection mandate.

Only direct debits issued in writing will remain valid after 1 February 2014. In future, your account statements will provide you with additional information such as the creditor identifier and a mandate reference (e.g. an invoice number or a membership number of the association). New direct debits will use SEPA mandates, standardised in all SEPA countries.

No. Direct debit mandates only have to be re-issued if the payee explicitly requests this from the customer.

As with the previous direct debit collection mandate, you are able here to arrange payments to be made to a payee. If you are the payee, agree a suitable mandate for this purpose and collect the payment using the SEPA Core Direct Debit. You can use the SEPA Core Direct Debit if your payment partner's bank also supports this scheme. DenizBank AG is part of the SEPA Core Direct Debit Scheme.

If an amount is ever debited from your account and you do not agree to it, you can object to it within a period of 8 weeks from the date of the debit entry (due date). You have the right to demand reimbursement of the direct debit amount without being required to state any reasons.

We will attend to the conversion of your standing orders and bank transfer slips on your behalf.

No, DenizBank AG will automatically attend to the IBAN and BIC conversion of the reference account (e.g. for direct debit payment collections or savings deposits).

No, there will be no change to your online banking log-in data (account number and PIN). Please continue to use your current details!

FAQ Corporate Customers

If you are paying an invoice, then you can read the IBAN and BIC from your business partner's invoice or letterhead. If you are unable to find the information you need from there, please contact your business partner directly.

As a payee or direct debit creditor, you will need a creditor identifier (or CI) to use the Euro direct debit based on the SEPA Direct Debit Scheme. This code is valid throughout all of SEPA, and it uniquely identifies you as a direct debit creditor.

In Germany you can apply to the Deutschen Bundesbank for your creditor identifier. If you have any questions, please contact your customer adviser – they will be glad to assist you further.

There is a new pre-printed form for Euro transfers, which you can obtain in our branch offices. You can also make payments easily using your online banking access.

There will no longer be pre-printed forms for national direct debit schemes, because submissions will usually be made electronically. As direct debit creditor, you can make your direct debit payment collections simply via your online banking account. Our advisors are ready and will to help you. Simply ask.

As of right now, you can use the new SEPA Direct Debit Scheme to collect payments - both inland and across borders using the SEPA Core Direct Debit, or if you are a corporate customer you can also use the SEPA B2B Direct Debit Scheme. The new SEPA Direct Debit Scheme is similar to that of the Austrian Einzugsermächtigung (direct debit collection mandate) and the Abbuchungsauftrag (a type of direct debit authorisation). It is based on direct debit collection mandates issued by the relevant payers.

The direct debit collection mandate can in future also be used for the SEPA Core Direct Debit. This negates any need for payees to go to the effort of obtaining SEPA direct debit collection mandates for existing debit collection authorisations. Another advantage is that under SEPA, direct debit payments under the direct debit authorisation scheme are now also insolvency-proof.

As is already the case with the SEPA Direct Debit Scheme, the reimbursement right under § 675x paragraph 2 BGB applies to the direct debit collection mandate procedure following the change. A standard reimbursement period of 8 weeks applies from the date of the debit entry – without any need for stating reasons. This also makes direct debit payments under the direct debit authorisation scheme insolvency proof.

No, direct debit creditors will be able to collect direct debit payments under the direct debit authorisation scheme as before.

For the payee the direct debit collection mandate is the instruction to collect amounts from the specified bank account via direct debit payment collections. For the bank of the payee, the direct debit collection mandate constitutes an instruction to redeem the direct debits of the payer. With the SEPA Core Direct Debit Scheme the direct debit collection mandate is known as the "SEPA direct debit collection mandate", in the SEPA B2B Direct Debit Scheme it is known as the "SEPA B2B direct debit collection mandate".

To ensure that direct debit payment collections are successfully executed, direct debit creditors are obliged to notify the payee of the amount and date of the payment before it is actually collected. This enables the payee to ensure that an appropriate sum is available on its account. If both parties have not made any other agreement, the payee must inform the payer of the pending direct debit 14 days ahead of its due date. A comparable procedure is already customary today. Alternative agreements can also be made between the payer and creditor regarding the pre-notification. For example, it may be sufficient to give notice of the direct debit by way of a comment on an invoice (as is the case today).

As a rule, the pre-notification must be dispatched at least 14 days prior to the due date. However there is the option for the payer and the payee to agree a shorter time period.

A SEPA Core Direct Debit will be authorised once the corresponding direct debit collection mandate has been signed. A SEPA Core Direct Debit is therefore deemed to be authorised in a legal sense even without pre-notification. As an obligation within a payments collection agreement, the dispatch of a pre-notification must be observed regardless. The payee should note the possible consequences of failure to issue a pre-notification, such as repayment due to lack of sufficient funds in the account or by way of a demand for the reimbursement of authorised payments. It is in the interests of the direct debit creditor that the payer be informed in good time prior to the due date or debit date of the direct debit payment collection, to enable it to ensure that sufficient account funds are available. This procedure likewise corresponds to current practice.

We will attend to the conversion of your standing orders and bank transfer slips on your behalf.

No, DenizBank AG will automatically attend to the IBAN and BIC conversion of the reference account (e.g. for direct debit payment collections or savings deposits).

No, there will be no change to your online banking log-in data (account number and PIN). Please continue to use your current details!

Everything you need to know about the IBAN!

Use our Smartphone-App and its practical IBAN calculator. Simply enter the account number and you're good to go! For more information or an

appointment please get in contact with us. Call our Contact Center 0800 4 88 66 00. We will be happy to assist you! Bildquelle: European Payments Council

If you have further questions, please call our toll-free number 0800 4 88 66 00 or submit us your question by filling out the

Contact Form.

New regulation effective since 2015: Church tax on Capital Gains

Since 1st January 2015 the church tax on capital gains (for example, interest, dividends) is automatically retained and paid to the tax-collecting religious communities.

In preparation for the church tax deduction, DenizBank AG is legally committed to check the religious affiliation of all customers with the Federal Tax Office (BZSt) once a year. The BZSt informs us about the members of a

tax-raising religious community with the “Church Tax Deduction Feature (Kirchensteuerabzugsmerkmal-KISTAM). The KISTAM provides information about the religious affiliation of the customers to a tax-raising religious community

and the existing valid church tax rate.

Right of objection and Blocking Notice

If you do not want to have the church tax levied by us, please contact the tax office and contradict the transmission of your KISTAM with a blocking notice. In this case, the declaration of the blocking notice shall be submitted

to the BZSt with an official form until 30 June of this year (§ 51a paragraph. 2c, 2e Income Tax Law “Einkommensteuergesetz”).

The BZSt then informs your registered tax office about your contradiction; your tax office will ask you to submit a tax return discloser.

For your information: The deceased´s accounts can´t be continued under the name of the deceased person. Therefore, after receiving the initial notification, we will send you the forms required for an account change or account

closure and, if necessary, request any missing documents.

Please note that the processing of the estate takes about four weeks.

In order to simplify the processing of the estate, we ask you in the case of an estate to submit the following documents (if they are already available to you).

Joint Account

Documents to be submitted by the co-accountholder:

Original or officially certified copy of the death certificate

Account Switching Form or Account Closing Request Form

If necessary, current proof of identity (if your proof of identity has already expired)

If necessary, exemption order

Individual Accounts

Documents to be submitted by the heir(s):

Original or officially certified copy of the death certificate

Original or officially certified copy of the opened will or certificate of inheritance

Current legitimisation of all heirs

Account Switching Form or Account Closing Request Form

If necessary, exemption order

Important legal information and footnotes:

Individual accounts are blocked until the estate is settled.

Please note that the current exemption orders end with the death of the deceased.

Current Time Deposits can be rewritten to the heir(s). If you want to cancel the term deposits early, then please note our Special Terms and Conditions Classic Savings / Online Savings.

The Deniz-Sparplan cannot be continued by the heirs. See the special conditions “Deniz-Sparplan”.

Legitimization can be done via the POSTIDENT (post-identification) procedure or by submitting certified copy of ID card. The POSTIDENT-Coupon can be downloaded at

Documents or sent to us per post.

If the heir already has an account in our house, an informal order is sufficient to have the deceased’s account rewritten to the heir´s current account.

In the case of an existing and valid power of attorney, the submission of the opened will or certificate of heirship is no longer required.

We are happy to accept certifications issued by our branches or your bank.

If you do not have an account in our bank and wish a rewriting , you can open the account via our Website here or on site in one of

our 3 branches and inform us in written form about the subsequent transfer of the estate via your newly opened account.