Skip to main content

Open New Account

Login

EN

DE

TR

DenizBank AG

×

Open New Account

Login

Saving & Financing

Time Deposit with Top Interest Rates

Daily Due Campaign 2026

More Savings Products

Deniz Savings Plan

Payment Account

Classic Savings

Send Money to Türkiye for Less

Financing

Instalment Credit

Transfers and Currency Exchange

Money Exchange

Türkiye Transfers

MoneyGram

Digital Services

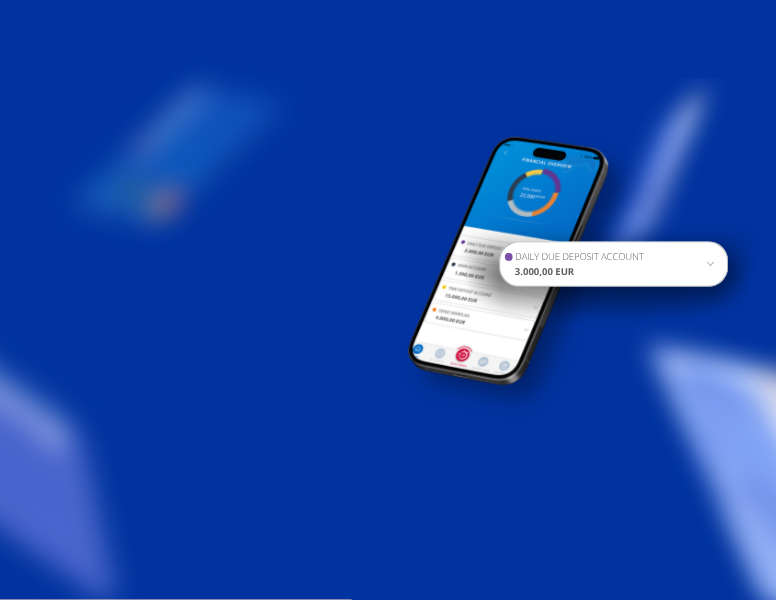

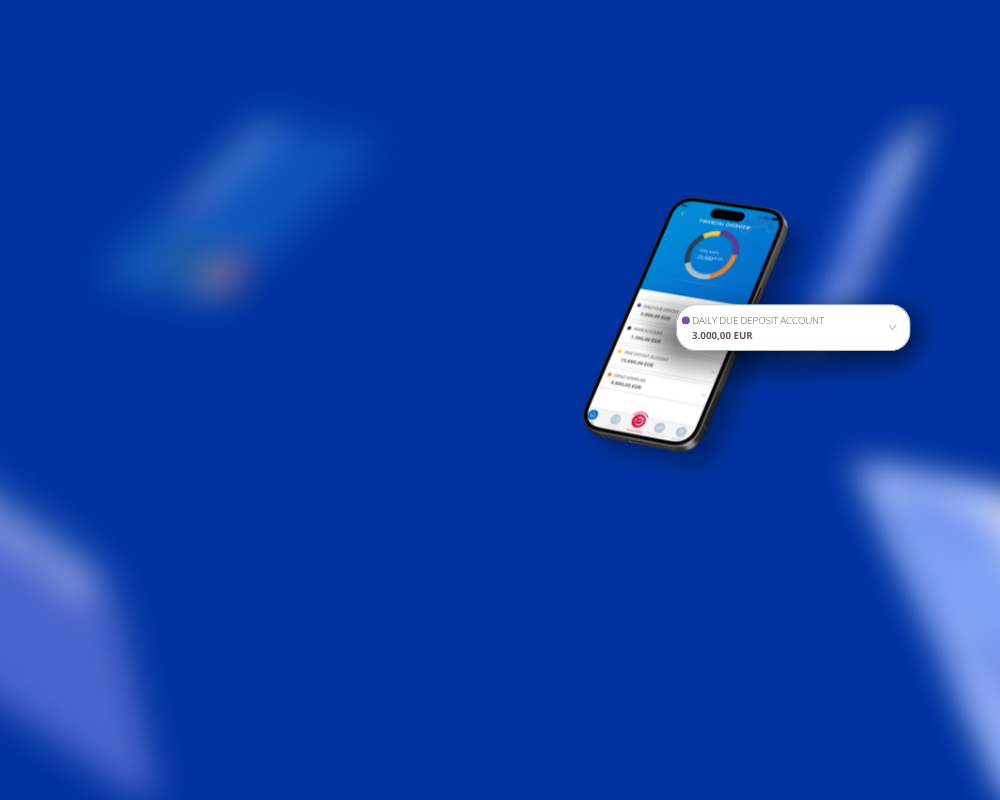

DenizMobile

Internet Banking

Open Banking

Info

Interest Rate Calculator

Business & SME

Loan Financing

Loan

Project Financing

Trade Financing

Transaction Banking

SME Solutions

Priority Banking

Deposit Products

FX Transactions

About Us

Company Philosophy

Shareholder Structure

DenizBank AG Management

Career

Media Center

Logos

Annual Reports

Sustainability

Disclosure Statement

Customer Service

About Us

Career

Digital Banking

EN

DE

TR

Enter search term

Press Enter or click the search button to search

Accessibility

Mode On

EN

DE

TR

Saving & Financing

Time Deposit with Top Interest Rates

Daily Due Campaign 2026

More Savings Products

Classic Savings

Deniz Savings Plan

Payment Account

Send Money to Türkiye for Less

Financing

Instalment Credit

Transfers and Currency Exchange

Türkiye Transfers

MoneyGram

Money Exchange

Digital Services

Info

DenizMobile

Internet Banking

Open Banking

Interest Rate Calculator

Business & SME

Loan Financing

Loan

Project Financing

Trade Financing

Transaction Banking

SME Solutions

Priority Banking

Deposit Products

FX Transactions

Open New Account

Login

The Banker Award

Deutscher B2B Award 2024

Digital Accessibility Badge

⏸️

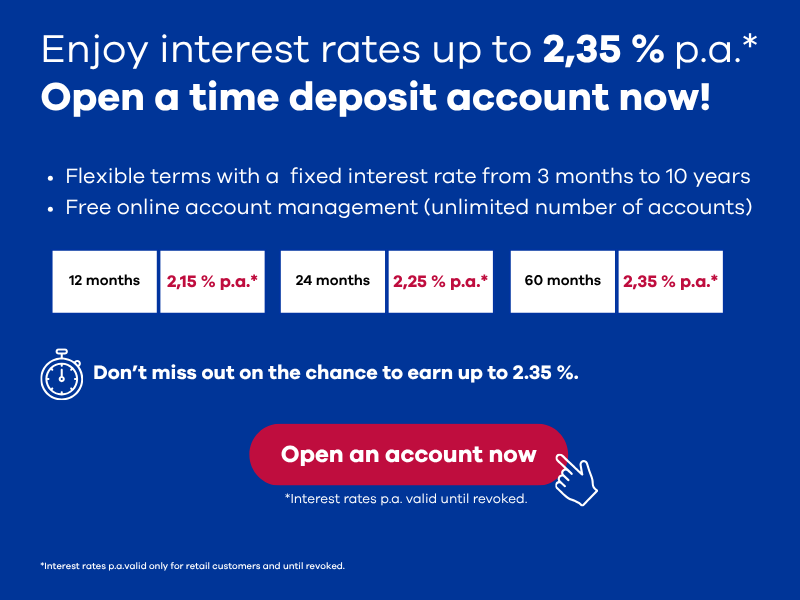

Get up to

2,50 %

p.a.!

For those who want more:

Earn up to 2.50 % p.a.* interest on Time Deposits.

Open Account Now

2.30 % p.a.*

for new

customers

Daily Due Campaign 2026

For New Customers: Secure Top Interest Rates with Our Daily Due Deposit Account.

More Info!

DenizBusiness – for Your SME

The Business Account for Smart Entrepreneurs. Profit from attractive interest rates!

More Info

Make an Appointment

Instalment Credit

An Instalment Loan to Suit Your Needs.

Further Info

Time Deposit Account

Open now

Deniz-Sparplan

Open now

Online Time Deposit Account

Get up to

2,50 % p.a. interest!

Further Information

DenizMobile

Fast and easy banking experience!

Learn More

Appointment

Branch Finder

Calculator

Contact Center